BY ADEREMI ABDUL

Nigeria’s economic growth and development hinge significantly on the strategic deployment of consumer credit. President Bola Ahmed Tinubu’s commitment to institutionalising consumer credit is evident in the establishment of the Nigerian Consumer Credit Corporation (CreditCorp).

This bold initiative has the potential to revitalise the economy, create jobs, and promote the growth of local industries.

Consumer credit is more than just cash disbursement; it is a powerful driver of economic growth, demand stimulation, and job creation. Globally, consumer credit has been linked to increased GDP, higher consumer spending, and millions of jobs. Nigeria must tap into this potential.

It is worth noting that in the past, consumer credit had been applied in Nigeria towards expanding the manufacturing and industrial sectors, creating employment opportunities, combating corruption, and catalysing economic growth. During the 1950s and 1960s, the government implemented policies that were aimed at stimulating industrial growth. Up until the 70s, consumer credit, primarily facilitated by private finance companies through hire-purchase agreements, was extensively used to finance the purchase of durable goods and capital equipment. This access to credit significantly boosted consumer spending, increased demand for locally produced goods, and supported the expansion of the manufacturing sector.

Advertisement

However, the introduction of the Structural Adjustment Programme (SAP) in the 1980s, which led to unrestrained importation and a high-interest rate regime, resulted in reduced credit availability and affordability for households. This shift severely impacted local industries that were mostly reliant on consumer credit, diminishing their ability to compete against cheaper imports and leading to the gradual decline of these industries, and ultimately resulting in the loss of millions of jobs.

At present, the consumer credit penetration in Nigeria remains critically low, comprising less than 10% of total private sector credit by banks and less than 3% of GDP. This was highlighted in the recent economic report by the Central Bank of Nigeria (CBN), comparing quite poorly to other peer African economies such as South Africa (40%), Kenya (10%), Egypt (12%) and Morocco (30%).

This limited penetration is predominantly focused on cash loans, with minimal strategic use of consumer credit to drive the productive sectors of the economy.

CreditCorp aims to address the current low consumer credit penetration – less than 10% of total private sector credit and less than 3% of GDP. Our strategy focuses on three key pillars: credit infrastructure, cultural re-orientation, and capital. The mandate of CreditCorp is to reverse this trend by removing structural, market, and policy barriers that are hindering the growth of consumer credit in Nigeria via the aforementioned three key pillars.

Advertisement

Firstly, we will strengthen credit infrastructure by collaborating with financial institutions, credit bureaus, and regulatory bodies. This helps to increase the number of consumers included in credit databases and while also improving the quality of credit information.

Secondly, we will promote financial literacy programmes to educate consumers on responsible lending and borrowing practices. This cultural shift is crucial for the sustainability of the consumer credit system.

This will also help to change the historical perception among some consumers that consumer credit is some type of a government social welfare programme, with minimal or zero obligation to repay.

Thirdly, we will provide wholesale lending to expand consumer credit reach, particularly to underserved households. To attract local and international wholesale capital, we will offer guarantees that mitigate lending risks. The strategy is to transition from full reliance on public budgets to attracting local and international wholesale capital by offering guarantees that mitigate lending risks.

To avoid fueling mass importation of foreign goods, we will align consumer credit expansion with the President’s “Buy Made-in-Nigeria” campaign. Our credit guarantees will support industries manufacturing within Nigeria, creating a virtuous cycle where increased consumer demand leads to higher production volumes, achieving economies of scale and ultimately resulting in lower prices for consumers. In other words, CreditCorp is committed to establishing a balanced and sustainable consumer credit system that supports local industries, enhances purchasing power, and contributes to economic growth and stability.

Advertisement

With the right approach, consumer credit can be a game-changer for Nigeria’s economy. We must seize this opportunity to unlock economic growth, empower citizens, and promote the rebirth of competitive ‘Made-in-Nigeria’ goods and services.

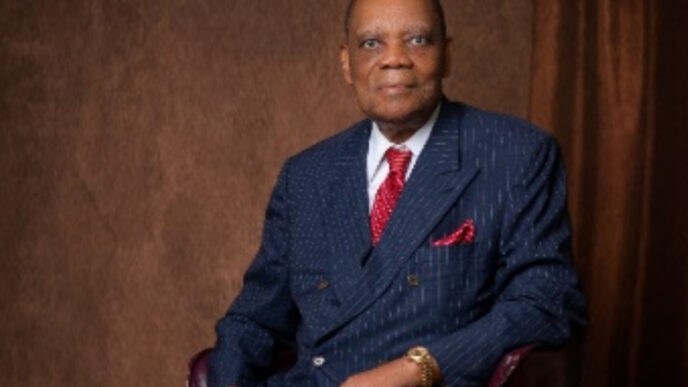

Otunba Aderemi Abdul is the chairman of the Nigerian Consumer Credit Corporation.. He can be contacted via [email protected]

Views expressed by contributors are strictly personal and not of TheCable.

Add a comment