BY FIYIN OSINBAJO

AN OVERVIEW OF CRYPTOCURRENCY

A blockchain is a digital ledger of transactions that is duplicated across a network of computer systems. Cryptocurrencies are digital payment systems that rely on blockchain technology to verify transactions. They can be used as a medium of exchange for goods services and do not require a central authority as governance is performed through a distributed consensus of the currency’s users.

Over the past few years, global attention has shifted to cryptocurrencies due to their potential to enable fast and cheap transactions while opening up possibilities for innovation in sectors such as telecommunications and finance. This interest has led to a large influx of capital into the cryptocurrency market, which is now valued at over one trillion United States dollars.

Advertisement

THE UTILITY OF DIGITAL ASSETS

Bitcoin is currently the world’s largest cryptocurrency; It enables peer-to-peer transactions between users, which can be settled in a matter of minutes regardless of the physical distance or difference in the banking/financial systems of their users’ countries of domicile. Currently, one of the most considerable barriers to commerce and trade is the movement of money due to the high cost and complicated processes involved when making payments through banks and other traditional financial institutions. For instance, international transactions are settled mainly through the SWIFT protocol, which provides an interface for banks worldwide to transfer money in various currencies. However, this can be done far more efficiently through cryptocurrency due to the potential for globally available, uniform methods of exchange.

To give context, most banks charge between 1-2.5% for international transfers. For a $500m transfer bank charges may go up to $5m. A Bitcoin transfer of the same amount will not exceed $500.

Advertisement

CRYPTOCURRENCY IN NIGERIA

Globally, technology has created a nexus of opportunities that have enabled economic growth, wealth creation, and poverty reduction. Nigeria’s large youth population coupled with rising internet adoption and smartphone penetration have made it a force to be reckoned with in the technology space. We currently stand at a crossroads regarding technology adoption, and many have suggested that in the present internet age, technology holds the potential to propel Nigeria to sustained growth and development.

Nigerians caught on to the cryptocurrency trend early on, and many were able to create opportunities for themselves and the country through cryptocurrency trading and service provision. Research has shown that in 2020 alone, over $400,000,000 (190 billion naira) worth of cryptocurrency was traded by Nigerians; a large amount of this volume was processed by Nigerian exchanges. For instance, Buycoins, an indigenous cryptocurrency exchange, had $141,395,605 traded on its platform in 2020 alone. The company had previously raised $1.2 million from foreign investors to expand its operations. Indigenous exchanges provide value to the country through tax revenues as well as the added benefit of making Nigeria a stakeholder and avid competitor in the one trillion dollar cryptocurrency market.

THE CBN BAN

Advertisement

The Central Bank of Nigeria recently instructed banks to identify and close accounts of cryptocurrency transacting entities. CBN’s decision is based on its understandable concerns that : Cryptocurrencies by creating an unregulated person to person financial system that often guarantees anonymity can facilitate criminal activity, that many other countries and at least one well known investor has made pronouncements warning against the use of cryptocurrency and that cryptocurrencies neither have intrinsic value nor do they create value The CBN’s decision will have a number of repercussions on cryptocurrency trading in Nigeria and the economy as a whole, some of these issues are discussed below.

NIGERIA’S POSITION IN THE GLOBAL TECHNOLOGY INDUSTRY

Prior to the ban, Nigerian companies had begun gaining a foothold in the cryptocurrency industry and put up stiff competition to foreign service providers. In effect, the CBN ban has made the operation of these companies illegal, thereby removing them from the one trillion-dollar market where they had thus far created value. The immediate effect of this will be the loss of millions of dollars of revenue to foreign competitors. Furthermore, cryptocurrency exchanges, like many other custodial services, operate on the basis of trust, which many may have difficulty recovering due to the abrupt nature of the halt in trading services. The decision may also affect affect the inflow of foreign capital to the Nigerian technology industry due to a perception of unfriendly and inconsistent policies.

THE POTENTIAL FOR FACILITATION OF CRIMES

Advertisement

While it is true that the relative anonymity offered by certain cryptocurrencies could be used for unlawful activity, the reality is that illegal transactions occur mainly through privacy coins, which allow senders and receivers to remain anonymous with different levels of privacy, such as hidden wallet addresses and transaction balances. These were not mentioned or addressed in CBN releases on this issue. It is important to note that the majority of cryptocurrencies exist on public blockchains as transparency underpins their utility, this makes them a poor choice for illegal activities.

National enforcement agencies can easily perform forensic audits of blockchains to reveal the identities of anonymous users committing illegal acts. Several countries have used this and similar methods to track down individuals who conduct illegal activities through cryptocurrency

Advertisement

Recently, privacy coins have been a major focus of regulation in countries around the world. For instance, in South Korea and Japan, the trading of privacy coins has been banned. This resulted in exchanges domiciled within these countries delisting these coins and not permitting further trading. A similar action in Nigeria would have gone a long way to curb illicit transactions as indigenous exchanges are under the control of the SEC and could have been restricted from dealing in privacy coins. As earlier noted, since the ban was placed exchange traded volume has fallen while peer to peer volume which the regulatory authorities have no control over has risen exponentially.

ADDRESSING CONCERNS RAISED BY THE CBN

Advertisement

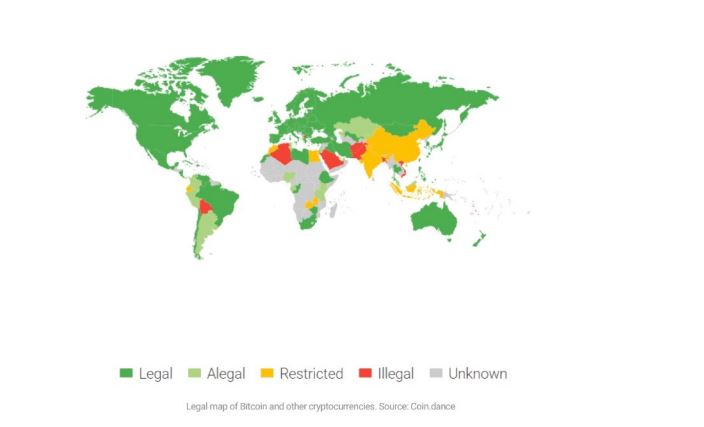

The CBN argued that many other countries have prohibited cryptocurrencies and that at least one notable investor has warned against their use. This is only partially so. The whole truth is that a majority of countries have allowed trading and put legislation in place to ensure investor protection. The map below shows countries where cryptocurrency trading is legal in green and illegal in red.

Advertisement

Also cited in the CBN’s report was a remark from Warren Buffet that cryptocurrency is a gambling device and a mirage because many buy it not as a means of payment but hoping they can sell it for higher than they bought. Again this presents a largely one-sided argument. Institutional interest in cryptocurrency has never been higher.

– Elon musk has fiercely advocated for cryptocurrency usage; his company (Tesla) recently bought $1.5 billion worth of bitcoin and has said that the currency will be accepted as a payment method for their products.

– Deutsche Bank recently said that “while only a decade old, digital currencies have already been shown to have the potential to radically change payments, banking, central banking and the balance of economic power.”

– Bill gates also holds the view that “Transforming the underlying economics of financial systems through digital currency will help those in poverty directly, and it will also support a host of other development activities, including health and agriculture,”

– Grayscale, a publicly traded investment management firm, launched cryptocurrency trusts, which enable institutional investors to gain exposure to digital assets. The company currently has over $30 billion of cryptocurrency assets under management, primarily owned by companies and high net-worth high individuals.

The CBN argued that cryptocurrencies have no intrinsic value and neither do they create value.

Fiat currencies such as the Naira and dollar are believed to have value due to the backing by respective governments and the trust individuals have in these governments. A statement by the US Federal Reserve of St. Louis stated that: “Bitcoin is not the only currency that has no intrinsic value. State monopoly currencies, such as the U.S. dollar, the euro, and the Swiss franc, have no intrinsic value either. They are fiat currencies created by government decree. The history of state monopoly currencies is a history of wild price swings and failures. This is why decentralised cryptocurrencies are a welcome addition to the existing currency system,” Paper currency replaced trade by barter because it was a more efficient medium of exchange and addressed problems of trust and reciprocity.

Cryptocurrencies are a more efficient medium of exchange due to the transparency, speed and lower transaction fees which they provide. In any event , the decentralised nature of cryptocurrencies makes it almost impossible to stop their usage. Even though Nigeria has banned cryptocurrency, there is no way to stop the movement of digital assets within the country as there is no central authority that issues these currencies. Instead, there is a decentralised network that operates through millions of

servers spread around the world. For Nigeria to stop cryptocurrency trading within the country, it would need to shut down every server around the world that processes cryptocurrency. In the few days since the ban, Nigeria has risen to the country with the second-largest volume of peer-to-peer bitcoin transactions in the world. Before the ban, most of this volume was traded through indigenous exchanges that paid tax in Nigeria and were being monitored and regulated by the SEC. So the question is whether more robust regulation could not at least save the baby from the rejected bath water? Other jurisdictions have approached the issues in this more preservatory way.

The United States has taken a two-pronged approach to cryptocurrencies. Firstly, cryptocurrencies are allowed to be traded within the country; this is guided by a regulatory framework for currencies and exchanges. Secondly, the country’s securities and exchange commission created a cyber unit that prevents misconduct and enforces sanctions on erring players in the industry.

The US SEC’s oversight has built confidence and created a relatively safe operating environment where consumers and service providers are adequately protected while improprieties are closely monitored. This resulted in an influx of capital to cryptocurrencies and service providers domiciled within the united states. ICE, the New York stock exchange parent company, launched Bakkt in 2015; it enables futures trading of bitcoin and allows institutional players access to the market. In 2020, over $12 billion worth of bitcoin was traded through bakkt.

The Nigerian Securities and Exchange Commission had previously released guidelines for service providers within the cryptocurrency space. The operation of Nigerian exchanges allowed a level of oversight of digital assets traded within the country. If the SEC noticed fraudulent transactions being passed through an exchange, it could easily place a ban on the exchange and investigate the source of funds, which would have either been deposited or withdrawn through a bank as part of a particular transaction or set of transactions.

CONCLUSION

Cryptocurrencies offer Nigeria an opportunity to cement its place as a knowledge based economy and attract the investment needed to stimulate growth. The CBN’s ban threatens Nigeria’s competitive positioning in the global technology industry and sends a negative signal to foreign investors who provide Nigerian technology companies with much needed capital. This paper argues that rather than being banned, cryptocurrencies should be allowed and closely regulated to curb illicit activities.

Fiyin is a 24-year-old technology entrepreneur. He graduated with an MSc in Management of Information Systems and Digital Innovation from the London School of Economics and a BA/Qualifying Law Degree in Law and Business studies from the University of Warwick.

Views expressed by contributors are strictly personal and not of TheCable.

Add a comment